Week ahead

We leave behind an eventful May, but June is expected to bring plenty more news for markets.

Next week, investors will be closely watching activity data from the eurozone, where economic confidence has been improving on the back of strong consumption and more stable business activity. The Markit purchasing managers’ index (PMI) and retail sales for May will question the sustainability of this positive trend. Data on first-quarter unemployment and May’s inflation readings will gauge signals from the region’s labour market, which should remain tight despite some recent softening. Investors shouldn’t fear any surprises from next week’s European Central Bank policy meeting, as interest rates are poised to remain unchanged.

In Asia, the focus is on China PMIs, which are likely to have taken a hit from recent trade news, albeit offset by local policy stimulus. In the US, markets await a particularly busy week amid the release of May’s PMIs and retail sales, as well as April’s construction spending and factory orders. Investors will be eager to see the extent to which business activity has been hit by trade wars rhetoric. We also look forward to May’s non-farm payrolls, unemployment rate and average earnings growth, with the job’s market expected to remain strong and income growth to advance further.

Chart of the Week

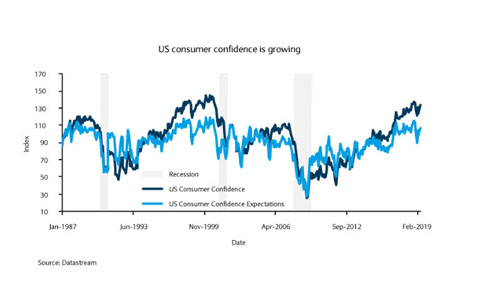

US consumer confidence supports growth outlook

The US consumer is not only the driving force behind the domestic economy but, arguably, the global economy too. Therefore, indicators assessing consumers’ health are closely monitored by market participants. The Conference Board US Consumer Confidence Index increased to 134.1 in May. The Present Situation Index, which is based on consumers’ assessment of current business and labor market conditions, increased from 169 to 175, near to 18-year highs.

Despite the negative spectre of trade wars, consumers’ optimism continues to benefit from declining unemployment, wage increases, low interest rates and tax cuts. The US unemployment rate of 3.6% is the lowest in 49 years and compares to above 10% in October 2009. We expect labour market improvement to persist over the next 18 months with the unemployment rate declining to 3.2% by the end of 2020.

Pay growth of 3.2% year on year is less than expected at this point of the economic cycle, but continues to run comfortably ahead of the rate of inflation. Low interest rates make it cheaper for consumers to service debts such as mortgages and tax cuts have boosted disposable income. We believe household consumption will continue to support growth for some time and therefore maintain our 2.8% growth forecast for the US economy for 2019.

Ceremonies have been taking place in Paris to commemorate the tenth anniversary of the attacks of 13 November 2015. 132 people lost their lives and ov...

Read More

Read More

France’s parliament is continuing to debate the draft 2026 national budget, and several measures under discussion could have a direct impact on foreig...

Read More

A man is in a critical condition in hospital after being found with wounds to his throat in Nice

Read More

US President Donald Trump has taken aim at France during a Fox News interview this week, saying that the United States has “had a lot of problems with...

Read More

Numerous commemorative ceremonies for Armistice Day have been held in our region and throughout France...

Read More