Week ahead

Markets are braced for a busy week ahead as more second-quarter (Q2) gross domestic product (GDP) and corporate earnings numbers are published. That said, the main economic news will be concentrated in select geographies.

In the US, the key figure to look for is the Q2 GDP advance reading. The reading is going to show a slowdown from the previous quarter number. Nonetheless, it will confirm that the US economy is still resilient despite reaching a record 10-year expansion earlier this month.

While backward looking, GDP data will give an important signal on the health of the US economy ahead of July’s US Federal Reserve policy meeting and in anticipation of a new round of US-China trade talks. The IHS Markit flash purchasing managers’ index (PMI) readings for July are also out next week, providing the market with a more timely indication on the health of the manufacturing part of the economy.

Expectations are that the recent contraction in manufacturing activity will come to a halt and services will stay resilient. Investors will also scrutinise June’s existing and new home sales data to assess the state of the housing sector.

In the eurozone, the European Central Bank meeting scheduled for 25 July is the main event in the spotlight. The central bank remains ready to ease policy after citing “heightened uncertainty” in the region, with markets pricing-in a possible deposit rate cut as early as this month. Investors will closely monitor July’s flash consumer confidence index and IHS Markit’s flash PMIs after May’s industrial production came out better than anticipated. That said, we forecast activity to remain muted although services should continue to look healthier than manufacturing.

We expect a quiet week in China and the UK with no major economic events scheduled. On the political front, we impatiently await the result of the Conservative Party leadership race on 22 July, which will see Boris Johnson or Jeremy Hunt emerge as Britain’s next prime minister.

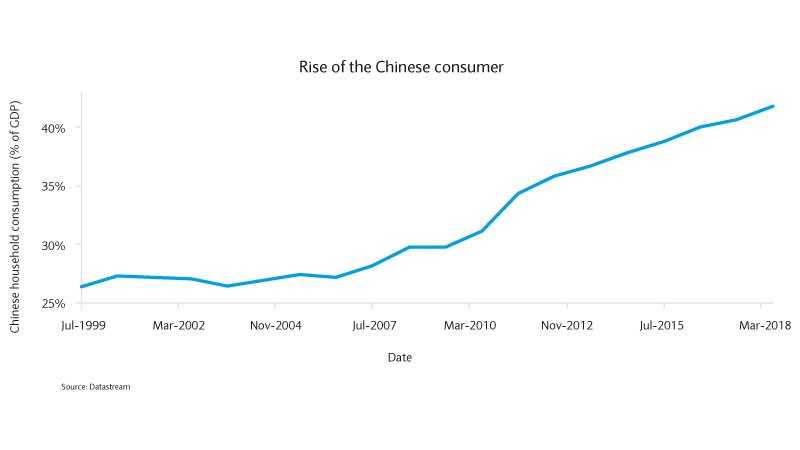

Chart of the week

Chinese retail sales: spend, spend, spend

This week’s second-quarter Chinese gross domestic product data showed retail sales growing at 9.8% year on year (yoy). The figure comfortably beat expectations, accelerating from the 8.6% yoy growth registered in June (although these figures were partly boosted by rising auto sales ahead of new environmental tariffs coming into force).

Historically we have thought of China as an arena for state investment and a manufacturing powerhouse. However, increasingly China is transitioning into a domestic consumption-led economy. In turn, the country’s retail sales trends are becoming ever more important to global growth prospects and market sentiment.

Chinese household spending power has risen rapidly over the past two decades as average wages have surged and its middle class continues to rapidly expand. (The World Economic Forum estimates China’s middle class will be 65% of all households by 2027). Domestic household consumption as a proportion of gross domestic product has risen from 26% twenty years ago to 42% today. Improving product supply chains, rapid digitalisation and rising urbanisation are also likely to support domestic demand in the future.

China is already the world’s largest market for cars, computers and mobile phones, the country boasting 1.4bn mobile subscribers. Furthermore, Chinese consumer spending on products and services shot up to $4.7tn in 2017, from £.3.2tn in 2012, according to the National Bureau of Statistics.

A range of international brands are already profiting from Chinese consumers’ rising demand for products and services, most notably in the luxury goods sector. Research shows that one in three of all luxury purchases around the world are made by a Chinese consumer. Lower price differentials with other countries, a reduction in import taxes and crackdown on unofficial suppliers have also helped to drive mainland China’s designer goods sales.

Several people have been taken into custody after a shooting in the centre of Nice yesterday. The victim was shot in the head on rue de la Buffa ...

Read More

Read More

The French government has announced a prohibition on mobile phone use in six prisons

Read More

A sharp blast of Arctic air is set to hit the Côte d’Azur this weekend, with temperatures dipping to –4°C in parts of the Alpes-Maritimes and the Var....

Read More

Two men and a woman from Beaulieu-sur-Mer have been appearing in court today as part of a judicial investigation into suspected money laundering and t...

Read More

Monaco celebrated its National Day on Wednesday with a blend of religious tradition, military honours and public festivities. The day began with a Te ...

Read More