Week ahead

With the fourth-quarter earnings season kicking in, investors will be paying close attention to next week’s macro data.

On Monday, the UK is expected to report relatively tepid gross domestic product (GDP) growth for November, after avoiding a “technical recession” in the third quarter (Q3) and seeing the weakest year-on-year growth rate since 2010.

In the eurozone, and the UK, the final December inflation reading is out on Tuesday. Both readings are likely to reflect the reversal of negative base effects for energy, the flash reading for the eurozone being up 0.3 percentage points to 1.3%.

Germany publishes the ZEW economic sentiment index. With market optimism over a “bottoming-out” of weak economic data, the index should provide some insight into whether this is surfacing.

In the US, investors will be able to better assess the resilience of the economy. December’s industrial production readings will signal whether there was a pick-up in manufacturing, as evidenced by survey data. Furthermore, the US Federal Reserve’s Beige Book, published on the 15th, should give more insight on economic conditions.

Turning to China, the country’s trade balance figure will be the first indicator published since the “phase one” US-China trade deal agreed in December. Industrial output and retail sales data should hint at the initial impact of trade tension de-escalation. China also reports its Q4 GDP data, with the market anticipating annual growth of 6.0%.

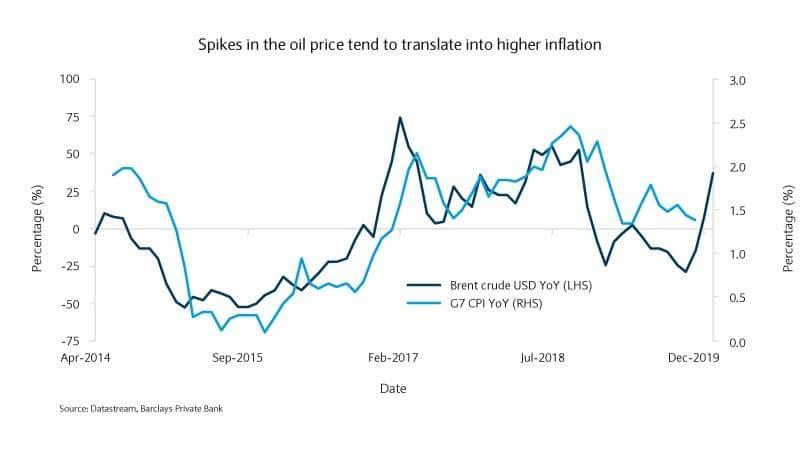

Chart of the week

Time to consider US inflation linked-bonds?

Tensions between the US and Iran have unexpectedly risen over the past week. This has led to fear of further sanctions being imposed on Iran and the lower oil output this would entail. The consequence has been a strong rise in the price of oil over the past few days.

Given oil’s heavy weighting in the consumer price index (CPI) basket, there is likely to be upward pressure on inflation.

The US inflation market has re-priced (to some extent) inflation expectations as a result of the shock. But it appears to remain of the view that inflation will stay lower for longer, with 10-year US break-evens (the difference between nominal and inflation-linked bond yields) at 1.75%.

Whilst such a view is plausible, it also means that the bar for upward surprises to inflation is low and two factors in particular could mean renewed and somewhat sustained inflationary pressures.

First is resilient US economic data. US non-farm payroll numbers have been notably strong, with 236,000 jobs created in November and housing data has also been encouraging. Demand-pull, upward, forces on inflation rates could surface off the back of this.

Secondly, in the first half of 2020 the US Federal Reserve is reviewing their inflation targeting framework, which could increase the prospect of a more relaxed inflation framework.

In light of both the low bar for inflation and the relative strength of upward surprises occurring, US inflation-linked bonds appear attractive.

All football fixtures scheduled for Sunday in the Alpes-Maritimes were postponed after the department was placed on an orange alert for heavy rain and...

Read More

Read More

A truck has collided with a tram in Nice this morning. The accident, on Line 1 of the tramway on Avenue Jean Medecin, happened at about 9.30am...

Read More

A woman in her early thirties has been killed after being hit by a car while walking on the A570 motorway near La Crau in the Var. The incident occurr...

Read More

Ceremonies have been taking place in Paris to commemorate the tenth anniversary of the attacks of 13 November 2015. 132 people lost their lives and ov...

Read More

France’s parliament is continuing to debate the draft 2026 national budget, and several measures under discussion could have a direct impact on foreig...

Read More